Brussels Builds Infrastructure for Digital Euro Confiscation as Cash Limits Tighten

The EU's new cash limits take effect just as the ECB launches its digital euro pilot, creating a ratchet mechanism that progressively erodes financial privacy while building the technical infrastructure for state control of money.

By July 10, 2027, Europeans will face a new reality at checkout. They can no longer pay for goods or services with more than €10,000 in cash when one party operates professionally. Purchases between €3,000 and €10,000 will require mandatory identity verification. The same month brings the European Central Bank's first digital euro pilot — a system with proposed holding limits of €3,000 to €4,000 and programmable infrastructure that Réka Kérész, a law student at Széchenyi István University, warns can embed state control directly into the mechanics of money. Brussels is systematically making cash inconvenient through Regulation (EU) 2024/1624 just as the ECB prepares its digital euro. The result is a ratchet mechanism designed to progressively erode financial privacy and economic freedom.

The stakes become real where citizens actually shop. ECB data shows 81 percent of point-of-sale payments fall below €25, yet the new €3,000 identification threshold and €10,000 cap will reshape everyday commerce. Crypto-asset transfers face even lower due diligence at €1,000. Member states may impose stricter national limits. The regulation takes effect automatically across all 27 member states without national transposition, overriding countries like Germany and Austria that previously had no cash limit at all.

The ratchet mechanism represents the most important structural reality of this transition. Belgium demonstrates that cash limits never remain static once established. The country steadily lowered its cash payment ceiling from €15,000 to €3,000 over successive legislative periods. That pattern proves a simple truth: once the state establishes the principle that it can restrict private cash transactions, those limits tighten. Belgium's restrictions now include prohibitions on cash purchases of real estate and scrap metal, with fines ranging from €250 to €225,000 for violations. "Once the principle is established that the state can limit private cash transactions, there is a strong tendency for those limits to become progressively stricter," notes the Foundation for Economic Education. "European countries themselves demonstrated this pattern when they still controlled these rules nationally."

Brussels embeds this tightening trajectory into a single binding framework. The EU is not merely setting one limit. It is constructing a mechanism that ensures limits will only move downward from here.

The timing of these restrictions aligns precisely with the ECB's digital euro rollout. Brussels published its digital euro pilot plan for the second half of 2027 in October 2025. The ECB received over 50 payment service provider applications in 2026 and aims for first issuance in 2029. The AMLR cash restrictions take effect July 10, 2027. "It is difficult to believe that it is mere coincidence that these restrictions are scheduled to take effect in July 2027 at roughly the same time the European Central Bank plans to launch the first pilots of the digital euro," FEE states. "Cash becomes inconvenient and potentially risky at the same time digital money is presented as the practical alternative."

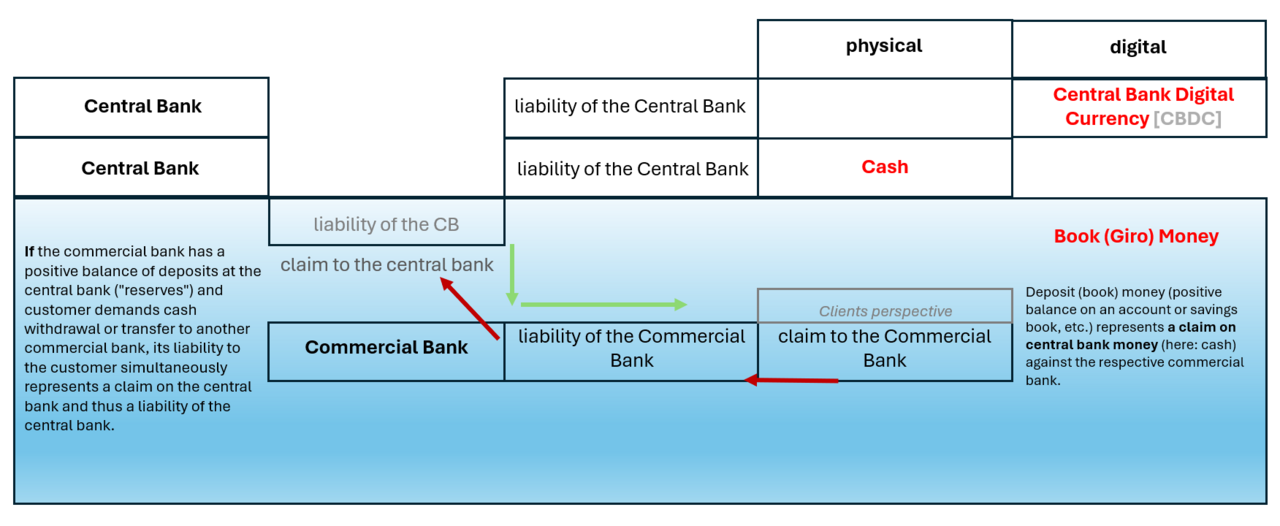

Programmability represents the most consequential technical feature of digital currency. China's People's Bank of China explicitly designed its digital yuan to be programmable and tested expiring money in its 2020 Suzhou pilot. Participants received funds with expiration dates. Money had to be spent within a limited timeframe or it would expire. By January 2026, China's digital yuan had become the first interest-bearing central bank digital currency. Reply/ABI Lab research demonstrates that European banks themselves have already explored programmability use cases including spending constraints by product category, by time period, and by geographic area.

The Eurogroup has stated the digital euro "cannot be programmable" and that holders cannot be prevented from spending it on certain purchases or at certain times. The ECB FAQs echo this position. Constitutional Discourse argues that programmability is a legal and institutional choice, not a natural feature of digital money. "Programmability is not a natural feature of digital money; it is a legal and institutional choice," writes Réka Kérész of Széchenyi István University. "Whether transaction limits, spending conditions, or expiry dates are embedded into a digital currency depends entirely on the normative framework governing its use."

China's implementation proves the technology works. The ECB's assurances lack historical credibility.

This programmable infrastructure serves as a prerequisite for what policymakers euphemistically call redistribution — the de facto confiscation of private savings. When money becomes traceable and programmable, the state gains the technical capacity to dictate where citizens spend, impose expiration dates on funds, and redirect private savings toward political priorities. The mechanism of confiscation shifts from legislation to code. The state no longer needs to seize property through overt decree. It can simply program the money to serve policy objectives. Traceable, programmable currency transforms the threat of confiscation from a political possibility into a technical capability.

The ECB proposes €3,000 to €4,000 per-person holding limits to safeguard financial stability. Ignazio Angeloni, former ECB Bank Supervisory Board member, finds that around €1 trillion of deposits could shift from bank deposits into digital euro accounts given these limits. The waterfall mechanism — where funds automatically flow from a user's bank account to the digital euro wallet when balance is insufficient, and excess funds above the holding limit flow back to the bank account — creates a system where consumers have little incentive to hold digital euros at all. "The ECB has argued that part of the justification for establishing the digital euro is to provide a monetary anchor to an increasingly digitalised economy, like the role cash plays today," states the Bruegel analysis. "But the waterfall approach and the link it establishes with a bank account reduces the need to replenish a stock of digital euros."

Brussels imposes uniform monetary behavior on countries with radically different cash cultures. The regulation overrides the principle that decisions should remain at the level closest to citizens. "Under the pretext of fighting money laundering, Brussels is imposing yet another form of forced harmonization that ignores the principle of subsidiarity," FEE argues. "The idea that decisions should be made at the level closest to citizens and national governments." Germany and Austria previously had no cash limit at all. Spain already restricts business transactions to €1,000. Greece limits to €500. The EU regulation harmonizes the baseline at €10,000 while allowing member states to go lower. That structure effectively empowers the most restrictive countries to set the direction for the entire bloc. Spain and Greece can now push Brussels to adopt their draconian standards as the European norm, because citizens cannot escape the restrictions by crossing to a neighboring country.

The taxpayer cost is staggering. Digital euro development runs €1.3 billion until first issuance. Annual operating costs from 2029 onward will reach €320 million. Taxpayers fund the very infrastructure that will erode financial privacy.

The digital euro Regulation has not yet been adopted by the European Parliament and Council as of June 2026. The ECB aims for legislative adoption in 2026 and first issuance in 2029. The ratchet mechanism means the €10,000 cash limit is almost certainly not the final ceiling. "The real risk is not an immediate transition to a cashless society, but a gradual shift in which regulatory decisions are embedded in technical systems without sufficient democratic oversight," Constitutional Discourse warns. "Once legal control is exercised through infrastructure, accountability must be designed into the system from the beginning." China's expiring digital yuan already demonstrates what is possible when money itself is programmable. Private savings become subject to state directives — not through legislation, but through the code that governs the currency.