Record Fed Split Marks End of Powell Era Amid Sticky Inflation

The Federal Reserve's most divided vote in 34 years exposes deep dysfunction as Jerome Powell exits with inflation above 3 percent, gas at $4.23, and rate cuts off the table for American families.

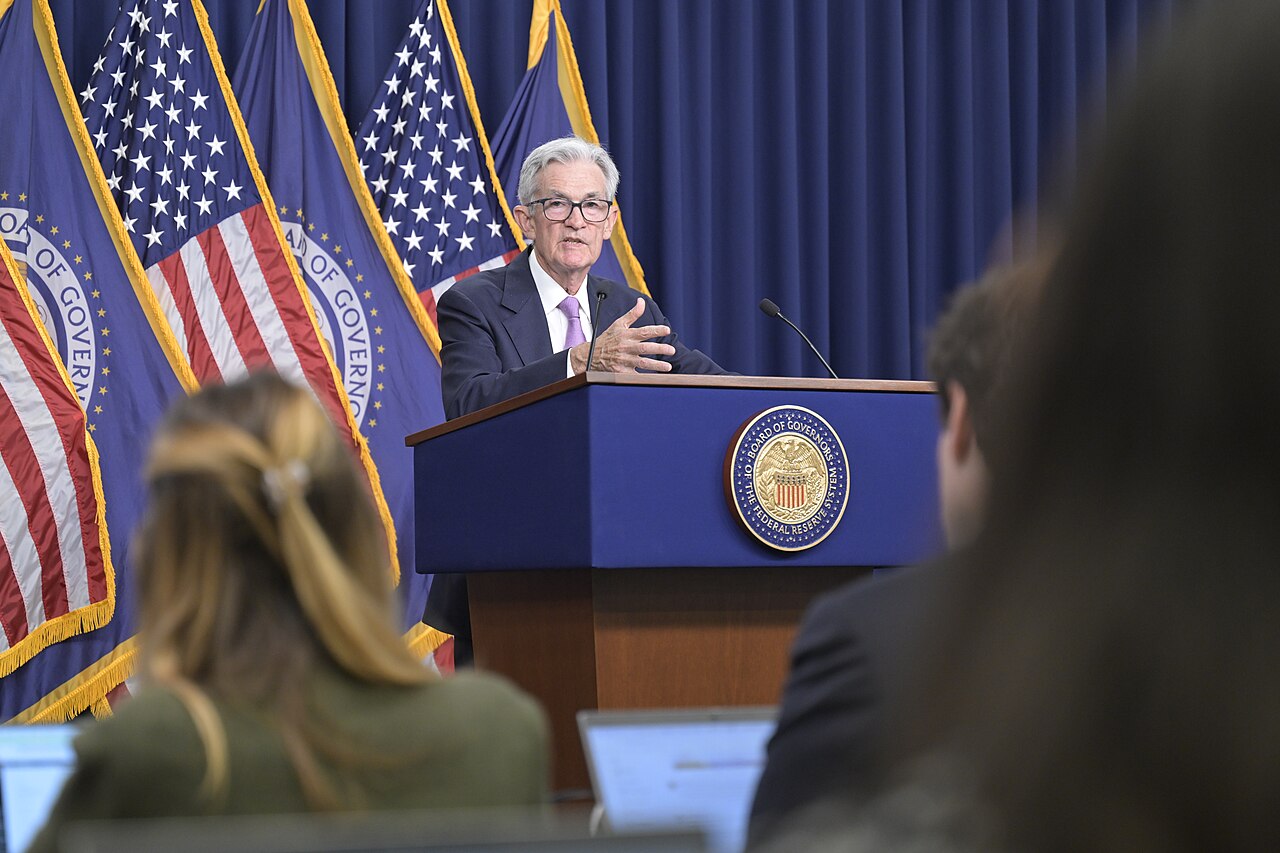

The Federal Reserve split 8-4 on its final interest rate decision under Jerome Powell, the most fractured vote in 34 years. That record dissent captures an institution that has weathered four successive crises yet left American families grappling with persistent inflation and mounting borrowing costs.

Powell departed on April 29 with inflation stuck above 3 percent, gasoline at $4.23 per gallon, and the deepest level of FOMC disagreement since 1992.

Three officials broke from the majority to hold rates steady at 3.5-3.75 percent, while a fourth dissented in favor of a quarter-point cut. That marks the most dissents since October 1992. Rate cuts are off the table for 2026. Americans will continue facing elevated borrowing costs while the Fed debates whether further rate hikes remain necessary.

The numbers tell the story of what consumers are paying for. March CPI rose 0.9 percent month-over-month to 3.3 percent year-over-year, the largest annual increase since April 2024. Energy prices jumped 10.9 percent. Gasoline surged 21.2 percent, pushing the national average to $4.23 per gallon. Core inflation held at 2.6 percent, but Purdue Agricultural Economics calls the flat food price reading a "temporary buffer, not a signal of insulation."

The Iran war has created the most challenging monetary policy environment for the Fed since the 1970s. The U.S. launched Operation Epic Fury and Israel launched Operation Roaring Lion against Iranian targets on Feb. 28, 2026. Iran closed the Strait of Hormuz to commercial shipping. Oil prices have surged 50-70 percent since the conflict began, with Brent crude reaching $118 per barrel in mid-March. The World Bank forecasts Brent oil to average $86 per barrel in 2026, up from $69, with energy prices projected to surge 24 percent.

Powell's final press conference served as an admission of institutional failure. "We've really had four supply shocks — you could actually say more than four, but at minimum, we had the pandemic, we had the invasion of Ukraine, we had the tariffs, and now we have Iran and the oil spike," Powell said. He warned that oil prices "haven't even peaked yet" and stated, "If we need to hike, we will, we will certainly signal that."

Markets have priced out rate cuts for the rest of 2026 and well into 2027. Claudia Sahm, creator of the Sahm Rule recession indicator, said: "Rate cuts are completely off the table. With inflation elevated, ongoing tariff pass-through, and an active war pushing energy costs higher, an early cut would require seven FOMC votes that Warsh does not have." Skanda Amarnath of Employ America added: "The reasons to cut have really diminished from where they were six months ago — actually quite the opposite."

The dissent vote breakdown reveals the Fed's internal chaos. Governor Stephen Miran, Trump's appointee, dissented in favor of a quarter-point cut, consistent with his pattern since joining the board. Cleveland's Beth Hammack, Minneapolis's Neel Kashkari, and Dallas's Lorie Logan dissented against the inclusion of an easing bias in the statement. They supported the hold but "did not support inclusion of an easing bias in the statement at this time," reflecting concerns about persistent inflation.

The Senate Banking Committee's 13-11 partisan vote to advance Kevin Warsh as Powell's successor signals a potential correction to eight years of inflation mismanagement. Warsh, a former Fed governor from 2006-2011, has called the 2022 inflation spike to 9.1 percent "the central bank's biggest policy mistake in four decades." He has advocated for "regime change" at the Fed, including a smaller balance sheet and revised communications.

Warsh said he would not be Trump's "sock puppet" and that "the president never asked me to predetermine, commit, fix, decide on any interest rate decision." During his confirmation hearing, however, Warsh declined to confirm he believes Trump lost the 2020 election when pressed by Sen. Elizabeth Warren, underscoring concerns about his independence from political pressure.

Sen. Warren, D-Mass., called Warsh a "Trump sock puppet who is so cowed by the president that he could not even say that Trump lost the 2020 election." She warned that advancing his nomination "will bring the president one step closer to completing his illegal attempt to seize control of the Fed and to artificially juice the economy."

Powell announced he will remain on the Fed Board of Governors until a Department of Justice investigation into the central bank's headquarters renovations is "well and truly over." U.S. Attorney Jeanine Pirro closed the probe but vowed she "would not hesitate to restart" it. Powell said the Justice Department provided assurances it would not reopen the investigation, but he is "watching the remaining steps in this process carefully." His decision blocks Trump from filling the seat with another appointee.

This was the first fully partisan FOMC chair vote in committee history, per Sen. Warren. The full Senate is expected to vote the week of May 11, with Warsh needing a simple majority. Republicans hold a 53-seat majority. The next FOMC meeting on June 17 is expected to be led by Warsh if confirmed. Ellen Zentner of Morgan Stanley noted: "A changing of the guard at the top of the Fed isn't going to change the central bank's calculus, or its process."

The record four-dissent vote in Powell's final meeting exposes an institution that failed to navigate four successive supply shocks, leaving behind sticky inflation above 3 percent, soaring energy costs, and the highest FOMC dissent since 1992. The transition from Powell to Warsh marks the first real opportunity for recalibration after years of policy missteps — and for the American families footing the bill.